Venmo is a digital wallet that offers a convenient way to send and receive money from friends and family, pay for goods and services, and share expenses. It’s part of the rapidly evolving digital payments landscape, providing a social twist to money transfers.

This article delves into Venmo’s pros and cons, highlighting its benefits while also shedding light on potential concerns and limitations.

What is Venmo?

Venmo was launched in 2009 by two college friends, Andrew Kortina and Iqram Magdon-Ismail, as a simple way for individuals to settle bills and other payments among friends.

It gained traction rapidly due to its unique blend of social networking and financial transaction capabilities.

In 2013, Venmo was acquired by Braintree, a payment gateway service provider, and subsequently became a subsidiary of PayPal in 2015 when PayPal acquired Braintree.

How Venmo Works?

Venmo works by linking your bank account, credit card, or debit card to your Venmo account. Once connected, you can use Venmo to pay anyone who has a Venmo account, as long as you know their username, phone number, or email.

Payments and requests for money are organized in a transaction history, which can be private or shared with your Venmo network.

When you receive money through Venmo, it stays in your Venmo account until you transfer it to your linked bank account.

Venmo’s Role in the Current Digital Payment Landscape

In the current digital payment landscape, Venmo has carved out a unique position. It’s not just a peer-to-peer payment app; it has effectively turned financial transactions into a social experience.

With the option to add comments and emojis to transactions and share them with friends, Venmo has integrated social media elements that make it more appealing, especially to younger users.

Furthermore, with businesses increasingly accepting Venmo as a payment method, it’s rapidly moving beyond its peer-to-peer roots.

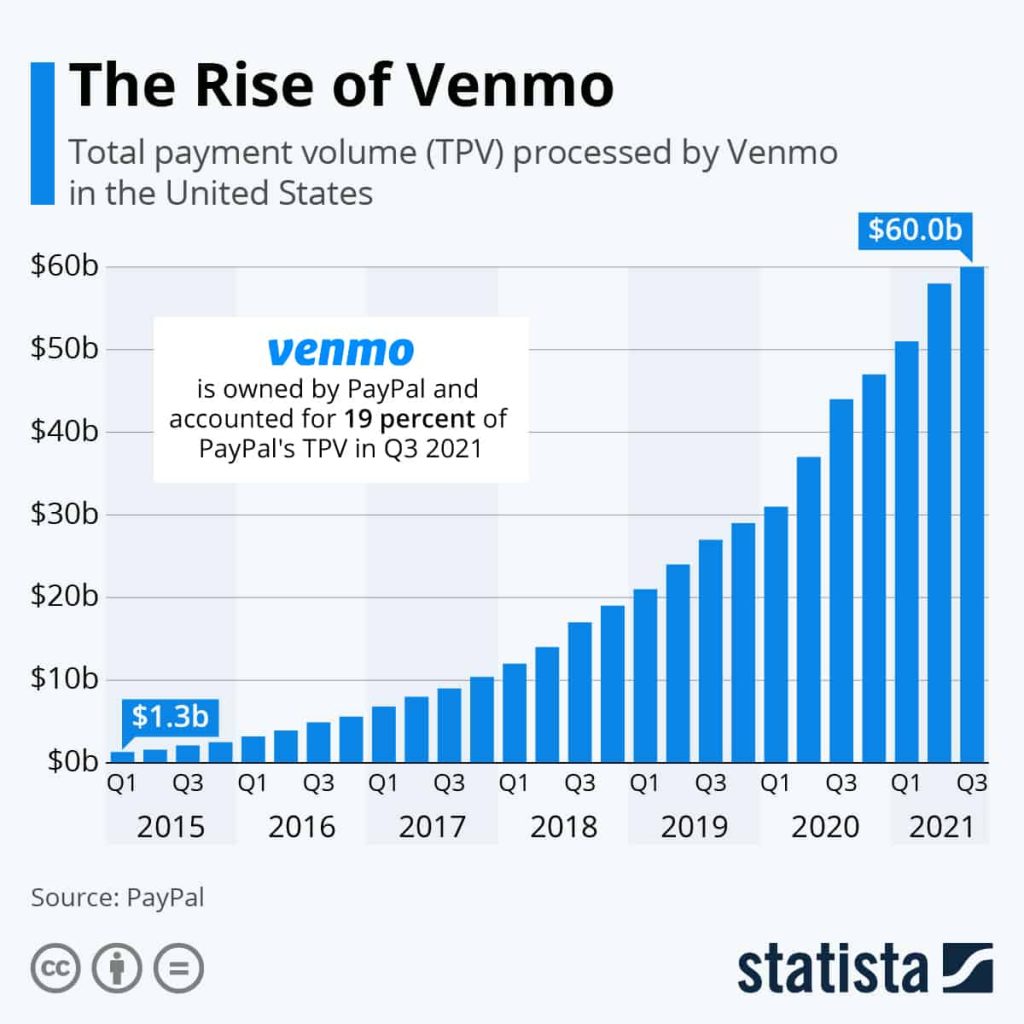

The platform had approximately 70 million users as of 2021, underscoring its significance in the digital payments space.

Pros of Using Venmo

Let’s explore the key advantages of Venmo.

Convenience

Ease of use: Venmo boasts a user-friendly interface that makes transactions straightforward. Whether you’re splitting a dinner bill or paying your half of the rent, Venmo simplifies the process.

Fast transactions: Transactions on Venmo are usually completed within minutes, making it ideal for immediate payments or transfers among friends and family.

Accessibility through mobile devices: With Venmo, your smartphone becomes your wallet. The app is available on both Android and iOS, making it accessible to almost everyone with a smartphone.

Social Integration

Integration with social media: One of Venmo’s unique selling points is its blend of finance and social networking. Users can link their Facebook friends list to their Venmo account, making it easy to find friends and share payment activities if desired.

Share transactions and comments: Venmo provides the option to share your transactions, along with comments and emojis, on a public feed. This social aspect can make payments feel less transactional and more personal.

No Transaction Fees for Most Personal Transactions

Venmo does not charge fees for basic services like sending money from a linked bank account, debit card, or your Venmo balance, or for receiving money and transferring it to a linked bank account. This makes it a cost-effective option for most personal transactions.

Purchase Protection

Venmo’s Purchase Protection program can cover users in certain cases where they purchased goods or services and have problems with the transaction.

For instance, if the goods never arrive or aren’t as described, the program may help recover the funds. However, it’s crucial to note that these protections often do not apply to personal transactions and have specific conditions and limitations.

Cons of Using Venmo

Let’s now examine the key disadvantages of Venmo.

Privacy Concerns

By default, Venmo shares your transactions on a public feed where anyone on the internet can see who you’re sending money to, along with any attached notes, unless you manually change your settings to private. This feature, although part of Venmo’s social appeal, can lead to privacy concerns.

Although Venmo does have security measures in place, the app stores user data which can be a potential target for hackers. Furthermore, if users are careless with their privacy settings or share sensitive information in transaction notes, they may expose themselves to privacy risks.

Limited International Use

Venmo is currently only available to users in the United States. Both parties in the transaction must be physically located in the U.S., and have a U.S. cell phone number, and a U.S. bank account. This makes Venmo less useful for international transactions or for non-residents.

Charges for Instant Transfers and Receiving Business Payments

While many transactions are free on Venmo, there are instances where fees apply. For example, there’s a fee if you want to transfer funds from your Venmo account to your bank account instantly.

Also, receiving payments for goods and services may incur a fee, and using a credit card to make a payment also incurs a fee.

Potential for Scams

Like any digital platform, Venmo can be used for fraudulent activities. Common scams include payment reversals, where a user sends money and then requests a chargeback from their bank, and phishing attempts, where scammers try to acquire sensitive information by masquerading as a trustworthy entity.

Users should only send and receive money with people they know and trust, review transactions carefully, and keep their app updated to the latest version for the most up-to-date security features.

Also, users should be cautious of any unsolicited communications asking for personal information or requesting urgent action.

Comparison with Other Venmo Alternatives

Now, let’s dive deep and compare Venmo with other alternatives to explore the Venmo pros and cons.

PayPal

Venmo, although a subsidiary of PayPal, differs in its social aspect and user-friendly interface designed for peer-to-peer payments. PayPal is more suited for business transactions, with wider international availability, but may not be as simple and straightforward for splitting bills among friends.

Zelle

Zelle, on the other hand, is directly integrated with many major banks, making it convenient for those who want to stick with their current bank. However, Zelle lacks the social aspect of Venmo and does not provide a digital wallet, meaning money is transferred directly between bank accounts.

Cash App

Cash App, similar to Venmo, provides a user-friendly platform for peer-to-peer payments and also offers features like investing in stocks or buying and selling Bitcoin. But Cash App also has limitations in international use, similar to Venmo.

Pros and Cons of Each Alternative

PayPal: PayPal’s advantages lie in its wide acceptance as a payment method by online retailers, its robust buyer and seller protections, and its international capabilities. However, it may not be the best for casual transactions among friends due to its fee structure.

Zelle: Zelle’s strengths are in its integration with banks and its speed, with transfers often happening instantly. But it lacks the social, fun aspect of money sharing and does not have an option for a digital wallet.

Cash App: Cash App, like Venmo, makes sending money easy and fun, and its ability to buy and sell stocks and Bitcoin sets it apart. However, it also lacks robust buyer protection and has fees for instant transfers and credit card payments, similar to Venmo.

Long Story Short

Venmo, with its user-friendly interface, quick transactions, social features, and absence of fees for most personal transactions, offers a unique and efficient way to handle peer-to-peer payments.

However, privacy concerns, the potential for scams, fees for instant transfers, and limited international use are significant considerations that potential users should weigh carefully.

In today’s digital age, where convenience and speed are paramount, Venmo’s appeal is evident. It addresses a real need for a simple, efficient means to handle financial transactions among friends and family.

It also adds a layer of social interaction to the typically mundane task of transferring money. However, like any financial tool, it is vital to understand its limitations and potential risks.

A mindful approach – being aware of privacy settings, being cautious with transaction comments, and only transacting with known trusted individuals – can go a long way in ensuring a safe Venmo experience.

If you found this article helpful and are interested in exploring similar topics, stay tuned for our upcoming pieces on digital financial tools.